A bank account is the first step to managing your money, but picking the right type is important. Savings Accounts and Current Accounts are the two most common options, each designed for different financial needs. A Savings Account helps people grow their money with interest. A Current Account is for businesses that need to handle many transactions. Knowing the key differences can help you make better banking choices.

In this blog, we will explain how both accounts work and which one is best for you.

What Is a Savings Account?

One kind of bank account that helps people save money safely and earn interest on their deposits is a savings account. It is intended for those who wish to increase their savings over time, keep their money secure, and have easy access to it.

Savings account is best for:

- Salaried people

- Students

- Housewives

- Elderly people

- Anyone looking to earn interest while gradually saving money

Savings account should be used for:

- Emergency funds and monthly savings

- Getting paid or having regular deposits

- Little, routine transactions

- Developing long-term financial self-control

- Safely parking extra cash

What Is a Current Account?

A current account is a kind of bank account intended for people and companies that must conduct high-value, frequent transactions. Although it typically doesn’t pay interest like a savings account, it’s perfect for business operations because it offers overdraft protection, limitless transactions, and easy cash flow management.

Current account is useful for :

- Owners and traders of businesses

- Professionals who work for themselves as freelancers

- Businesses, start-ups, and joint ventures

- Wholesalers, retailers, and service providers

- Businesses that handle a lot of transactions

A current account should be used for:

- Keeping track of daily business payments and receipts

- Managing frequent and sizable transactions

- Keeping cash flow stable for company operations

- When there are temporary financial shortages, using overdraft facilities

- Paying suppliers and getting paid by clients

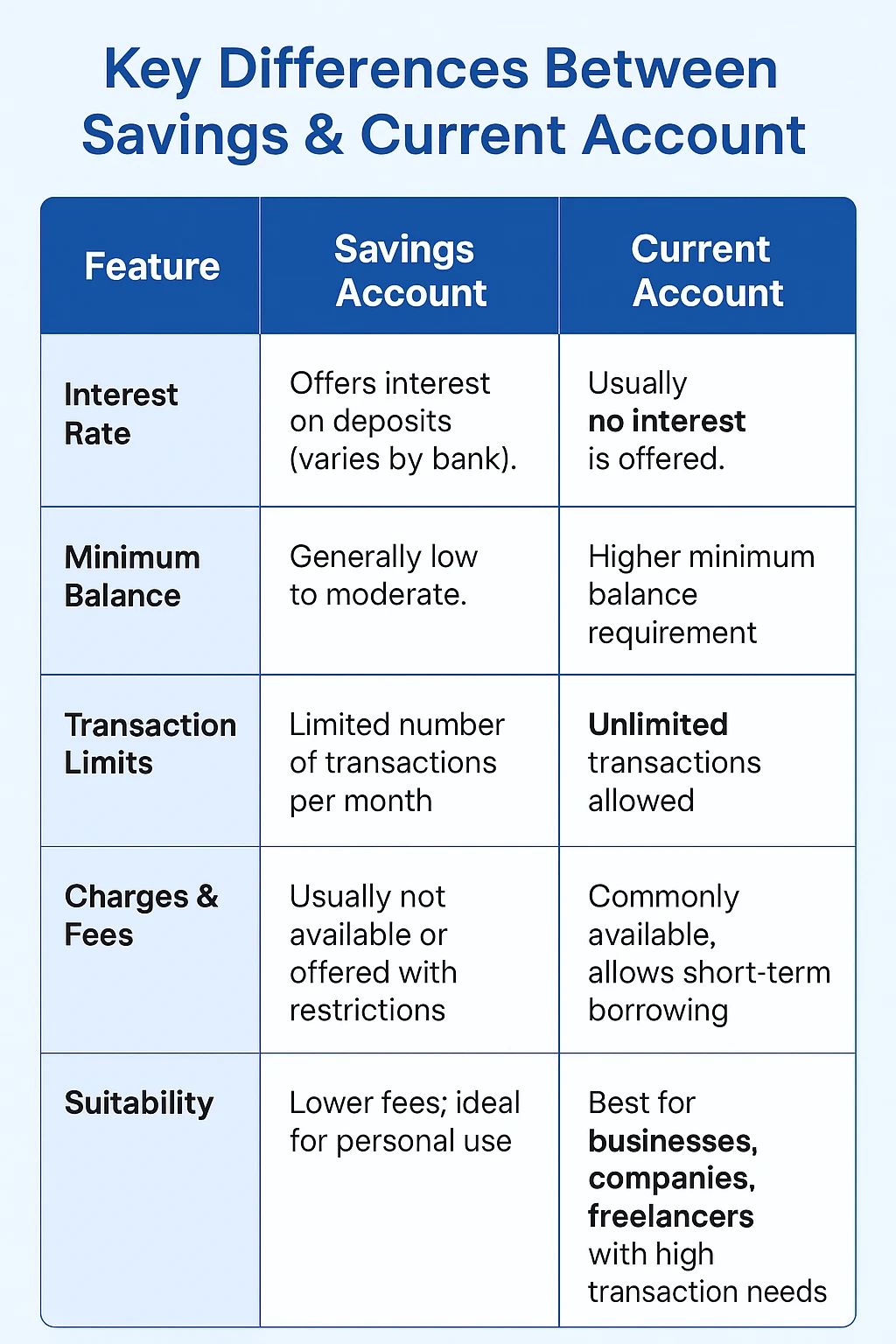

Key Differences Between Savings & Current Account

| Feature | Savings Account | Current Account |

|---|---|---|

| Interest Rate | Offers interest on deposits (varies by bank). | Usually no interest is offered. |

| Minimum Balance | Generally low to moderate. | Higher minimum balance requirement. |

| Transaction Limits | Limited number of transactions per month. | Unlimited transactions allowed. |

| Overdraft Facility | Usually not available or offered with restrictions. | Commonly available, allows short-term borrowing. |

| Charges & Fees | Lower fees; ideal for personal use. | Higher fees due to business-related services. |

| Suitability | Best for individuals saving money. | Best for businesses, companies, freelancers with high transaction needs. |

Features of Savings Account

1. Deposit interest

Your savings increase over time as a result of the interest you receive on the funds held in your account.

2. Minimal Requirement for Balance

Because most banks have low or moderate minimum balance requirements, families, salaried individuals, and students can all use them.3. Withdrawals from ATMs and Debit Cards

Debit cards are given to account holders so they can easily pay their bills, make purchases, and withdraw cash whenever they want.

4. Simple Mobile & Internet Banking

Net banking and mobile apps for bill payment, balance checks, fund transfers, and much more are included with savings accounts.

5. Limited Deals

Banks may restrict the quantity of free transactions in order to promote thrifty saving practices.

6. Safe and Secure Storage of Funds

Banking regulations safeguard your money, providing a secure location for both daily savings and emergencies.

7. Auto-Pay & Standing Instructions

You can set up automatic payments for EMIs, bills, SIPs, and recurring transfers.

Features of Current Account

1. Infinite Transactions

Current accounts are perfect for businesses with regular financial activity because they permit unlimited deposits and withdrawals.

2. Facility for Overdrafts

For temporary business needs, the majority of banks provide an overdraft facility that enables account holders to take out more money than their balance.

3. Balance Has No Interest

Since current accounts are meant for transactions rather than savings, they usually don’t offer interest.

4. Increased Requirement for Minimum Balance

Because of the wide range of services they offer, banks have a higher minimum balance requirement than savings accounts.

5. Quicker Collections & Payments

facilitates quick business transactions, including bulk payments, instant fund transfers, RTGS, NEFT, and IMPS.

6. Business Banking Tools & Cheque Book

Multiple check books, payment gateways, point-of-sale devices, and other business-oriented services are provided to account holders.

7. Higher Charges & Service Fees

These accounts often come with higher service costs due to unlimited transactions and premium business features.

Savings Account vs Current Account: Which Is Better?

1. Students

-

Best Option: Savings Account

-

Why? Low minimum balance, interest earnings, and essential services like ATM withdrawals and UPI payments.

2. Salaried Individuals

-

Best Option: Savings Account

-

Why? Ideal for receiving salary, saving monthly income, and earning interest.

-

Use Current Account Only If: You run a side business requiring frequent transactions.

3. Interest Rates

-

Savings Account: Offers interest (usually 2.5% to 6% depending on the bank).

-

Current Account: No interest or very minimal interest.

4. Minimum Balance Requirements

-

Savings Account: Low to moderate (₹0–₹10,000 depending on the bank & account type).

-

Current Account: High minimum balance (₹10,000–₹1,00,000+ depending on business type).

5. Transaction Limits

-

Savings Account: Limited free transactions per month; restrictions on cash deposits/withdrawals.

-

Current Account: Unlimited transactions—perfect for businesses with daily financial activity.

6. Charges & Penalties

-

Savings Account: Low charges; penalties for not maintaining minimum balance are also low.

-

Current Account: Higher fees for non-maintenance, cheque books, cash handling, and other business services.

7. Documents Required to Open a Savings Account

-

Aadhaar Card

-

PAN Card

-

Passport-size photographs

-

Address proof (utility bill, rental agreement, passport, etc.)

-

Basic KYC form

8. Documents Required to Open a Current Account

-

PAN & Aadhaar of proprietor/partners/directors

-

Proof of business (GST certificate, Shop Act, business registration)

-

Partnership deed or Memorandum of Association (MoA) / Articles of Association (AoA)

-

Address proof of business

-

Identity proofs of authorized signatories

-

Passport-size photographs

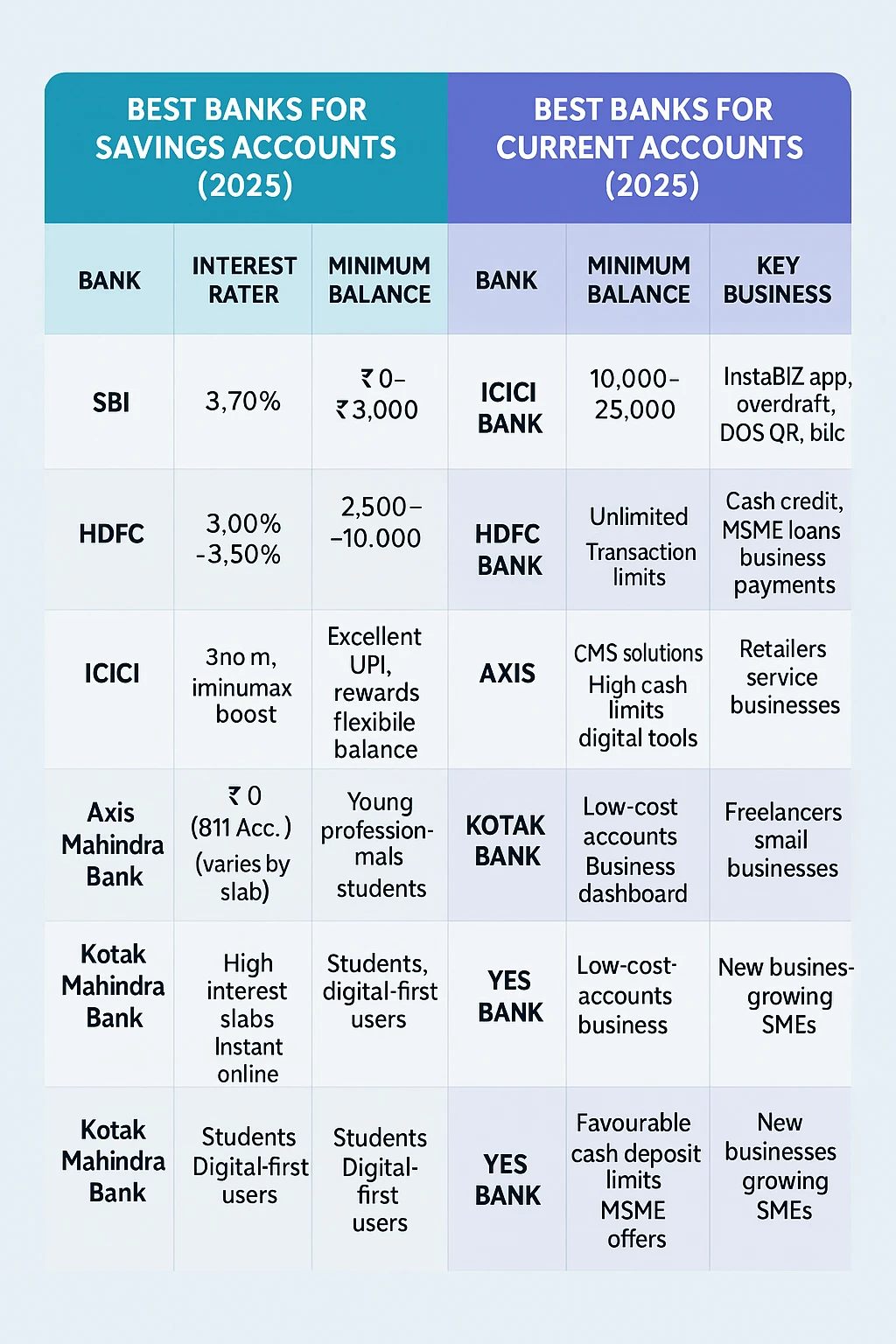

Best Banks for Savings Accounts in India (2025)

| Bank | Interest Rate Range | Minimum Balance | Key Features | Best For |

|---|---|---|---|---|

| SBI | 2.70% | ₹0–₹3,000 | Wide branch/ATM network, zero-balance accounts | Students, rural users, families |

| HDFC Bank | 3.00%–3.50% | ₹2,500–₹10,000 | Great mobile banking, premium debit cards | Salaried individuals, urban users |

| ICICI Bank | 3.00%–3.50% | ₹2,500–₹10,000 | Excellent UPI, rewards, flexible balance | Professionals, daily banking users |

| Axis Bank | 3.00%–3.50% | ₹2,500–₹10,000 | Fast onboarding, good digital services | Young professionals & students |

| Kotak Mahindra Bank | 3.50%–4.00% (varies by slab) | ₹0 (811 Account) | High interest slabs, instant online opening | Students, digital-first users |

Best Banks for Current Accounts in India (2025)

| Bank | Minimum Balance | Transaction Limits | Key Business Features | Best For |

|---|---|---|---|---|

| ICICI Bank | ₹10,000–₹25,000 | Unlimited | InstaBIZ app, overdraft, POS/QR, bulk transfers | SMEs, startups, enterprises |

| HDFC Bank | ₹10,000–₹25,000 | Unlimited | Cash credit, MSME loans, business payments | Retailers, service businesses |

| Axis Bank | ₹10,000–₹50,000 | Unlimited | CMS solutions, high cash limits, digital tools | Traders, wholesalers |

| Kotak Mahindra Bank | ₹10,000–₹50,000 | Unlimited | Low-cost accounts, business dashboard | Freelancers, small businesses |

| Yes Bank | ₹10,000–₹25,000 | High transaction limits | Favourable cash deposit limits, MSME offers | New businesses, growing SMEs |

Common Myths About Savings & Current Accounts

1. Current Accounts Are Only for Big Companies

Many believe only large businesses can open Current Accounts. In reality, freelancers, shop owners, startups, and small businesses can also open them.

2. Savings Accounts Always Give High Interest

Not true—interest rates depend on the bank and may be low or fixed. Some digital banks offer better interest than traditional ones.

3. You Can’t Use a Savings Account for Business

While possible, it’s not recommended. Frequent transactions may lead to charges, restrictions, or account monitoring.

4. Current Accounts Are Expensive to Maintain

Some banks offer affordable or low-cost current accounts, especially for small businesses and freelancers.

5. Savings Accounts Don’t Have Transaction Limits

Most Savings Accounts have limits on free ATM withdrawals, cash deposits, and branch transactions.

Savings Account or Current Account: Which One Is More Secure?

Both Savings and Current Accounts are equally secure because they are governed by the Reserve Bank of India (RBI) and protected under the Deposit Insurance and Credit Guarantee Corporation (DICGC).

Security Breakdown

Savings Account Security

-

Highly secure for personal savings

-

Protected up to ₹5 lakh per depositor (DICGC insurance)

-

Lower transaction volume reduces fraud risk

-

Ideal for storing emergency funds and savings

Current Account Security

-

Equally protected under ₹5 lakh DICGC insurance

-

Additional security tools for businesses like OTP-based payments, token devices, and dual authorization

-

High transaction volume means users must stay more alert.

FAQs: Savings Account vs Current Account

1. What is the main difference between a Savings Account and a Current Account?

Ans: A Savings Account is for personal savings and earns interest, while a Current Account is for businesses and supports unlimited transactions.

2. Can I use a Savings Account for business transactions?

Ans: You can, but it’s not recommended because frequent transactions may lead to charges or account restrictions.

3. Do Current Accounts offer interest like Savings Accounts?

Ans: No, most Current Accounts do not offer interest as they are designed for business transactions.

4. Which account is better for students?

Ans: A Savings Account—it offers low minimum balance, interest, and basic banking features.

5. Is there a minimum balance requirement for a Savings Account?

Ans: Yes, but it is usually low. Some banks also offer zero-balance accounts.

6. What documents are needed to open a Savings Account?

Ans: Aadhaar, PAN, address proof, passport-size photos, and basic KYC details.

7. What documents are needed to open a Current Account?

Ans: Business registration proof, GST certificate, PAN, Aadhaar, address proof, and authorized signatory documents.

8. Can freelancers open a Current Account?

Ans: Yes, freelancers and self-employed individuals can open a Current Account.

9. Which is safer – Savings Account or Current Account?

Ans: Both are equally safe and protected under DICGC insurance up to ₹5 lakh.

Conclusion

Choosing between a Savings Account and a Current Account depends entirely on your financial needs. If you are a student, salaried employee, or someone looking to save money and earn interest, a Savings Account is the best option. It offers security, interest earnings, and low minimum balance requirements.

On the other hand, if you are a business owner, freelancer, shopkeeper, or company needing high-volume transactions, overdraft facilities, and flexible cash flow, a Current Account is the right choice. It is designed specifically for daily business operations.

Leave a Reply